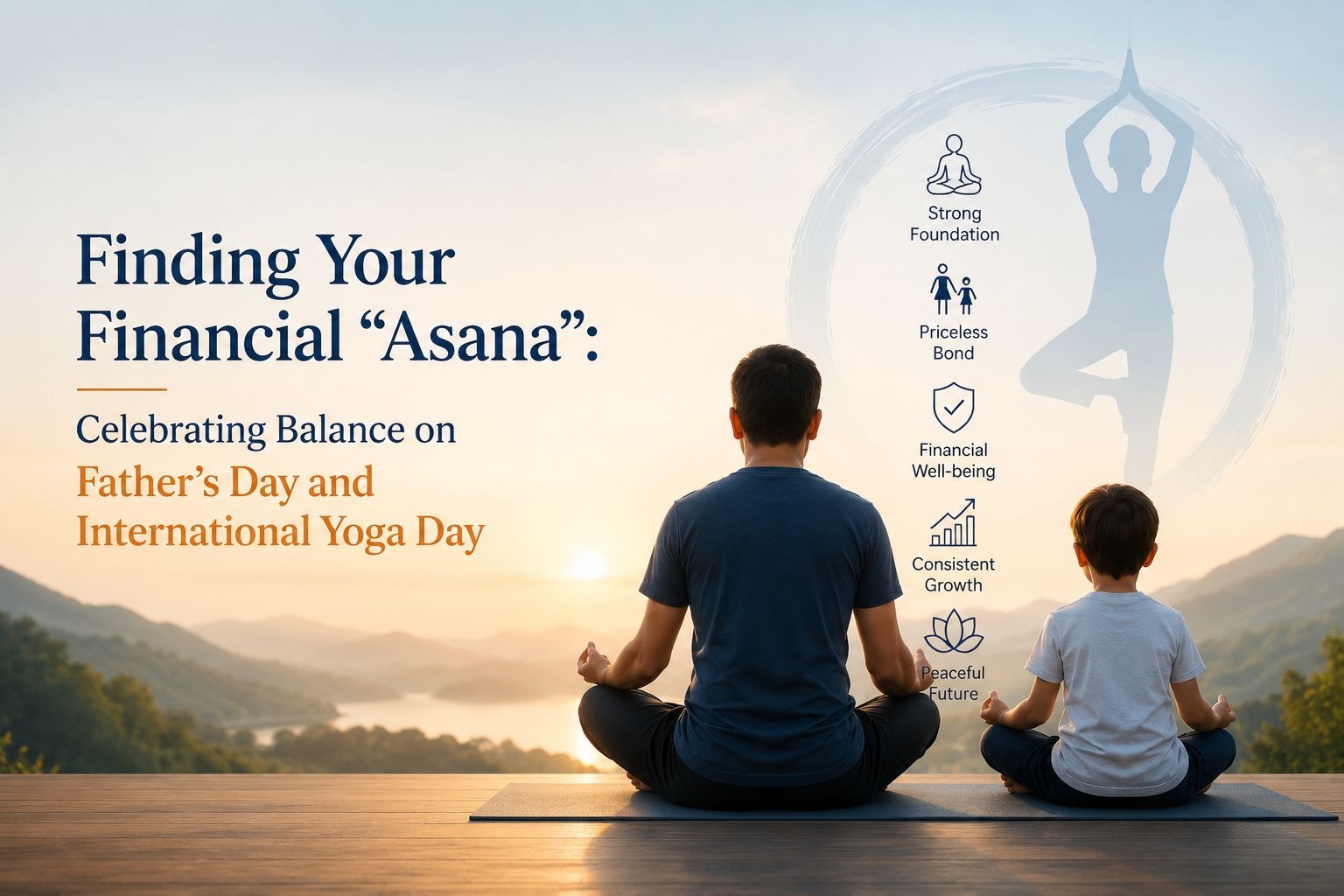

On June 21, 2026, we experience a rare and beautiful convergence of two celebrations: International Yoga Day and Father’s Day.

At first glance, mindfulness on a yoga mat and the protective guidance of a father might seem to have little in common with your investment portfolio. But if you look closer, both of these celebrations revolve around a single, powerful theme: Balance.

In Yoga, the perfect Asana (pose) is achieved when strength meets flexibility. In life, a father acts as the ultimate anchor—providing unwavering stability while encouraging us to grow and take risks.

Your financial portfolio requires this exact same harmony. To celebrate this unique day, let’s explore how the lessons of the yoga mat and fatherhood can help you master the art of asset allocation, secure steady returns, and find your financial peace of mind.

1. Equity and Debt

In Yoga, forcing your body into a difficult pose without a strong, grounded core leads to injury. Conversely, holding too rigidly to one position prevents growth. Your investment portfolio behaves the exact same way:

Equity is your Flexibility: It represents your reach, your growth potential, and your ability to outpace inflation over the long term. But just like a flexible yogi without muscle control, a portfolio 100% invested in equities is highly vulnerable to sudden market twists and volatility.

Fixed-Income is your Core Strength: Bonds, Non-Convertible Debentures (NCDs), and fixed-income assets are your muscles. They keep you upright, absorb macroeconomic shocks, and provide a reliable foundation of regular cash flow.

Achieving financial balance means ensuring your growth assets (Equities) are always supported by a robust, steady core (Fixed-Income). When equity markets experience a “market tantrum,” a balanced allocation ensures your overall wealth remains upright and unharmed.

2. The “Father” of Your Portfolio: The Grounding Power of Fixed-Income

Think about the role a father plays in a family. He is the protector, the quiet anchor who ensures the bills are paid, the future is secure, and there is always a safety net when life gets unpredictable.

In the financial world, high-quality bonds and NCDs play the role of the father. They don’t chase loud, speculative headlines. Instead, they do the heavy lifting of protecting your capital and providing predictable, compounding payouts.

The Three-Bucket Strategy For fathers looking to secure their family’s future—or for children looking to help their aging parents build a stress-free retirement—this strategy is highly effective. By keeping short-term needs in highly liquid, safe assets, and mid-term goals in stable, yielding instruments, you ensure your family never has to panic-sell equities during a market downturn.

3. Creating Balance in Today’s Economic Climate (June 2026)

Finding balance isn’t a static, one-time decision; it requires adjusting to the environment around you. Just as a yogi modifies their pose based on wind or terrain, smart investors must adjust their portfolios to the current macroeconomic landscape.

Right now, the Reserve Bank of India (RBI) has kept the benchmark repo rate steady at 5.25%. With domestic inflation projected at 5.1% for the financial year, keeping all your money in traditional bank fixed deposits (which are currently peaking at around 6.50% at major lenders.) might leave your real, inflation-adjusted returns barely scratching the surface.

To calculate your true progress, always remember the mathematical formula for your real rate of return:

True Progress Calculator

Find out what your investments are really earning after taxes and inflation.

Your Real Post-Tax Return

Your post-tax return is 7.00%. After adjusting for inflation, your wealth is growing.

To prevent inflation from quietly eroding your hard-earned wealth, you need safe, high-yielding fixed-income instruments to act as your portfolio’s anchor.

A Timely Opportunity for Your Portfolio’s Anchor

For investors seeking to add immediate, high-yielding balance to their portfolios, a highly anticipated corporate debt offering is opening for subscription:

| Feature | Details |

| The Issuer | Vedika |

| The Safety Net | Rated Infomerics A-/Stable, indicating a very high degree of safety and robust credit quality |

| The Yield | Offering highly attractive coupon rates up to 11.5% depending on the selected tenure |

With options for monthly, annual, or cumulative payouts, this NCD allows you to customize your cash flows to match your specific financial needs—whether that is a monthly “pension” for your retired parents or a compounding bucket for your child’s education.

Achieve Financial Serenity This June 21st

Yoga teaches us that “balance is not something you find, it is something you create.” Similarly, a father’s legacy of security is built through deliberate, disciplined actions taken day after day.

This Sunday, as you roll out your yoga mat or sit down to express your gratitude to your father, take a moment to look at your financial health. Are you overstretched in volatile equities? Is your capital being eroded by low-interest deposits?

Let us help you bring harmony back to your wealth. At Vedika Finserv, we specialize in crafting tailored fixed-income portfolios that act as a protective, rewarding shield for your family’s future.

Happy International Yoga Day & Happy Father’s Day!